In this comprehensive analysis spanning IPOs from 2019 to November 2023, our focus is primarily on evaluating the trends and performance of companies that went public during this period. Emphasizing a shareholder’s perspective, we delve into the intricate dynamics of IPOs, acknowledging that the fundamental goal at the outset is for companies to raise substantial capital during their initial public offering. While this immediate financial infusion is crucial, we recognize that long-term stock appreciation is a key expectation for shareholders post-IPO.

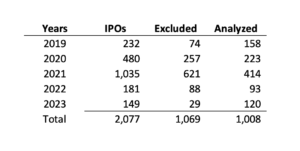

The sectors predominantly represented in the IPO landscape are Healthcare, Technology, and Consumer industries, with specific concentrations in Biotech, Medical Devices, Software, and Consumer Goods. Notably, the majority of IPOs price their shares in the range of $15 to $20, reflecting a common valuation approach during their market debut. A peak number of IPOs was reached in 2021 with a record of 1,035 companies going public. In contrast, in 2023 we experienced a notable decline with 149 IPOs, marking the lowest figure in the past five years.

Within the IPO landscape, Nasdaq emerges as the predominant listing platform, hosting approximately 75% of all IPOs, while the remaining 25% find listings on the NYSE and other markets. Our study covers a timeline of the last five years, including slightly over 2,000 IPOs. It is imperative to note that for the purposes of our in-depth analysis, we have deliberately excluded SPACs, Shell/Acquisition Companies, and entities that underwent mergers, privatization, or business closures. This approach ensures a focused examination of IPO trends and shareholder outcomes in a dynamic market environment.

Among the remaining 1,008 public companies that went IPO, only 200 have demonstrated a positive return, gauged by the cumulative increase in share price since their respective IPOs. It is noteworthy to acknowledge that companies going public in 2019 had a more time to realize share price increases compared to those entering the public market more recently. Within the context of this analysis, we designate these 200 entities as “successful companies.”

In our comprehensive examination, we meticulously scrutinized various metrics to discern patterns and commonalities among these successful companies in contrast to their counterparts. Metrics encompassed a wide spectrum, including revenue, net income, economic value, return on assets (ROA), return on invested capital (ROIC), earnings per share (EPS), growth rates, and an additional 120 metrics. Despite the breadth of metrics evaluated, the culmination of our analysis reveals a somewhat straightforward observation: these successful companies share a fundamental trait—they exhibit scale and tangible results. Scale is evident through increase in revenue levels achieved via sustained growth, while results manifest in positive EBITDA and/or free cash flow, emphasizing the pragmatic outcomes that contribute to their success.

Companies exhibiting positive returns to shareholders consistently outpace their counterparts with negative returns, showcasing a 2x superiority in both revenue and revenue growth. Simultaneously, these prosperous companies surpass their less successful counterparts by 3x in terms of net income and/or EBITDA. While this finding might seem somewhat anticipated, it strongly aligns with our earlier discussion on the importance of profitable growth and a clear path to profitability. The market sentiment emphasizes that an unwavering focus on growth, without due consideration for profitability within a reasonable timeframe, is not sustainable.

As an example, examining companies that went public in 2019 and achieved success reveals an average revenue nearing $2 billion, starkly contrasting with their less successful counterparts averaging $580 million. Similarly, companies successful in their 2020 IPOs boast an average revenue of $3.7 billion, significantly outshining their counterparts with an average of $600 million.

Delving into net income, companies that triumphed in their 2020 IPOs recorded a net income of $128 million, compared to a $100 million loss for their less successful counterparts.

Moreover, the 200 successful companies consistently outperform others in terms of return on assets (ROA), return on invested capital (ROIC), and return on equity (ROE), demonstrating a twofold advantage.

By further stratifying companies based on returns exceeding 100% against those falling below this threshold, another pattern emerges. Notably, the companies achieving returns higher than 100% exhibit a more pronounced trajectory of revenue growth, reaching 25%. In stark contrast, their counterparts yet to attain a 100% return demonstrate a comparatively modest revenue growth, standing at 15%. This underscores the importance of achieving significant revenue growth to achieve stock price appreciation.

Karuna Therapeutics (KRTX), creates and delivers medicine for people with psychiatric and neurological conditions.

IPO: $16, in 2019

Current Price: $214 or 1,230% increase

Shockwave Medical (SWAV), focuses on the development and commercialization of medical devices

IPO: $19 in 2021

Current price: $177 or 935% increase

Airbnb, provides housing rental for travelers around the world.

IPO: $68, in 2020

Current Price: $140, or a 107% increase

In assessing the landscape, it’s imperative to acknowledge the prevalence of failures in this analysis. Among the initial 1,008 companies scrutinized, a substantial subset comprising 186 entities are currently trading at less than $1 per share. It’s noteworthy that the average initial price for these companies was $9 per share. Collectively, these 186 companies raised $13.5 billion. It is obvious that investors, to date, have not realized any returns on this considerable capital infusion, emphasizing the challenges and complexities inherent in navigating the public market terrain.

In essence, companies that achieve the milestone of ringing the bell at the NYSE or at NASDAQ are in a different class, not all companies can achieve the size and scope to get to this level and raise millions of dollars for future growth. On the other hand, those investors are seldom compensated and in fact a lot of investors are never compensated for the risk of placing a bet on the management of these companies. For every success story (success defined from a stock appreciation point of view) there are 4 disappointments.